Reports are circulating in the British press that the Home Secretary (UK’s interior Minister) will announce an end to the so-called Golden Visa for UK immigrants. These Visas allowed High Net Worth individuals to buy a fast track to UK residency and ultimately citizenship.

A little known fact is one of the multitude of variables used by the UK pensions authority to calculate state pension liabilities involve both expected mortality AND the ratio that has on time spent working verses retirement.

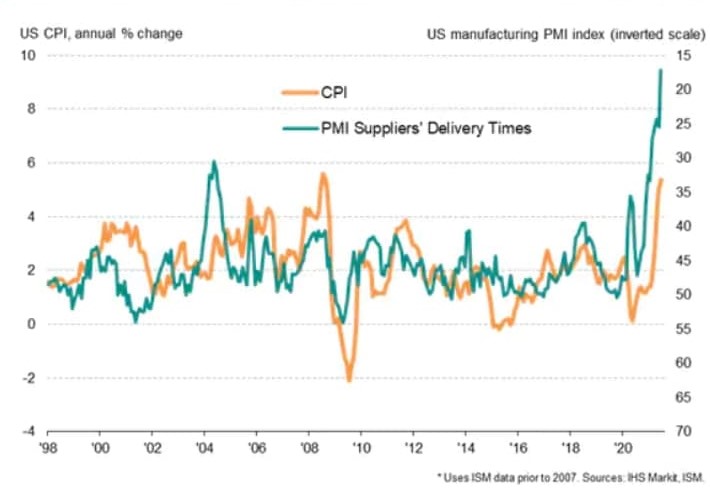

FITs are now live on Facebook. This week we discuss UK dividend opportunities, the inflation threat of PMI delivery times, crypto risks and two stock trades.

UK equities are trading at a discount to global peers of more than 40%. This has no equivalence within recent living memory. The UK is bouncing back from the twin hits of the Pandemic and Brexit, and with vaccination figures leading the way globally, it seems ripe for the UK economy to re-open and break out.

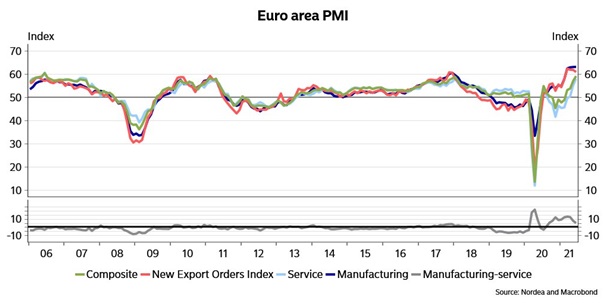

Not to be outdone, the usually anemic Eurozone has seen a raft of positive figures after positive figures.

We discuss the pet industry, specifically Trupanion stock and the ETF for the sector, PAWZ. We revisit UK's depressed valuations and Europe's increased PMIs. After reviewing the Blue Chip Portfolio, highlighting Nike's fabulous earnings report, we offer two 'rebound plays'.

Now National Insurance contributions – for British citizens including expats – are paid according to the type of CLASS of contribution that you are liable to make. Which CLASS is relevant to you can be the first complicated calculation.

If you approaching pension age and are resident in a low tax jurisdiction (Russia, for example), you could take advantage of the UK's flexible drawdown regime from age 55. If you are non-resident for tax purposes, although you might in future return to the UK to live, or indeed to another country, you may be able to receive the full value of your fund liability to UK tax and so without deduction of tax at source. By investing the proceeds properly, you could obtain tax free growth whilst you are outside the UK and then benefit from withdrawals of 5% per annum tax free when you are back in the UK.

Owners of second homes or buy-to-let properties must brace themselves for a seismic shift in how capital gains tax is paid, on top of the rule changes for non-residents who own UK property.

Scroll to Top

Наш сайт использует файлы cookie и похожие технологии, чтобы гарантировать максимальное удобство пользователям. При использовании данного сайта, вы подтверждаете свое согласие на использование файлов cookie. Узнать больше.